The China National Coal Association (CNCA) recently published its guidelines on developing the coal industry during the 14th five-year plan period (2021-2025). The guidelines are deemed to be close to the official plan, which is due to be published by the National Development and Reform Commission (NDRC) next year. According to the guidelines, China will continue deepening its supply-side reform, with a greater focus on improving supply quality.

Key points in 13th and 14th five-year plans

| 13th five-year plan | 14th five-year plan | |

| (2016-2020) | (2021-2025) guidelines | |

| by NDRC | by CNCA | |

| Annual coal output limit (Bt) | 3.9 | 4.1 |

| Annual coal consumption limit (Bt) | 4.1 | 4.2 |

| No. of coal mines | Around 6000 | Fewer than 4000 |

| Share of output from large mines (≥1.2 Mtpa) | Above 80% | Above 85% |

| Proportion of coal processed | Above 75% | Around 80% |

| Source: NDRC, CNCA |

Fewer mines

During the 13th five-year plan period (2016-2020), China aimed to reduce the number of coal mines to 6,000. It overachieved this target by cutting the number to below 4,700. It will continue to cut the number of mines, targeting a level below 4,000 in the next five years. We believe China can easily achieve this target by shutting down small mines in regions such as the southern provinces.

But greater output

While reducing the number of mines, China will expand annual domestic output, but limit to 4.1 billion tonnes in the coming five years. Inevitably, the country will keep replacing small mines with large mines in a few key producing regions.

We will likely see coal capacity and output peak at a national level towards the end of the 14th five-year plan period. As an essential part of the energy mix, coal demand is still growing to support the economy. The guidelines eye annual coal consumption amounting to 4.2 billion tonnes by 2025.

But the pressure to decarbonise is becoming more and more evident. The target to peak carbon emissions by 2030 is depressing coal demand. Consequently, we expect coal output to start to decline as demand shrinks approaching 2030.

With more advanced production technologies

Apart from replacing outdated capacity, the country will also strive to upgrade production technologies to support higher output.

The industry will continue to improve the level of mechanisation in mining. It also aims to develop nearly 1,000 mines using intelligent mining techniques. That means mines will be equipped with systems that strengthen information acquisition and technology, enabling more mechanised, automated and unmanned operations.

Tighter regulatory pressure arising from safety and environmental concerns is also part of enhancing production compliance. Miners’ awareness is improving as well. For instance, after Amendment XI to the Criminal Law of China came into force in March, companies can be held criminally responsible for any violation of provisions on safety management during production or operations. As such, it will become rare to see mines producing above approved capacity.

And lastly, the marketable coal product quality will be refined with a higher proportion of raw coal undergoing processing, including crushing, screening and washing.

Potential market vulnerabilities

Despite the industry improvements, variations at the regional level could be more severe. China has 14 major coal-producing regions. At the end of the 13th five-year plan period, these regions contributed more than 95% of coal output. China will further expand this share to more than 97% by 2025.

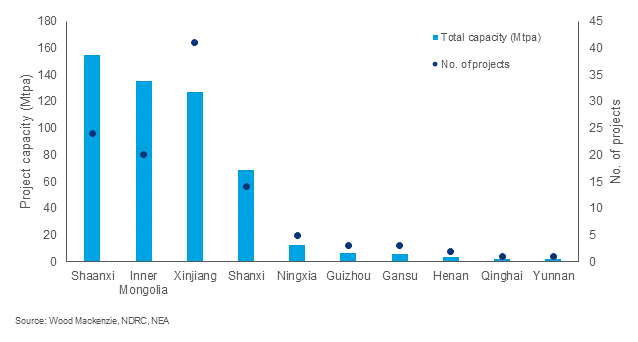

But not all regions will expand capacity. We expect to see capacity additions in Inner Mongolia, Shaanxi and Xinjiang – a continuation of the recent policy effort to approve projects in these regions. Meanwhile, capacities will either remain flat or edge down slightly over the next five years in the other regions. Consequently, we expect a higher degree of geographical concentration.

Project approvals (2017-2021 H1)

While coal production is relatively flat throughout the year, demand varies significantly at different times. The imbalance at the regional level due to geographical concentration may further add pressure to seasonal tightness. As such, although coal capacity will increase at the national level, there may still be a temporary shortage of coal and fluctuations in prices, especially in peak demand seasons or during disruptions to supply from any of the key producing regions.

And measures to address market volatility

To address the regional imbalance, China continues to encourage mergers and acquisitions in the coal industry, especially among state-owned enterprises. The more prominent producers can strengthen their regional supply chain and better meet the demand of end users. China is looking to establish 10 large coal producers, each with an annual output above 100 Mt, up from the current six big miners. Control over coal supply and logistics will strengthen as the industry concentration increases.

China also wants to strengthen its coal inventory system. In 2013, the NDRC identified 11 large bases for coal storage in places including coastal demand centres, coastal and river ports, and near key railway hubs. To enhance coal storage capacity, China announced further steps to build inventory, backed by the government or relevant companies. The NDRC recently unveiled a plan to make more than 200 Mt of coal inventory deployable by the government. In response, Hubei province, for example, is looking to expand its coal storage capacity to 16 Mt by 2025.

On top of that, the target inventory level held by coal miners and end users is around 400 Mt. The government will use regulations to manage the maximum and minimum levels. We expect inventory expansion will be a measure used to modulate effective supply in the market and therefore stabilise coal prices.

That said, the inventory target will be roughly 15% of annual coal consumption, and such a scale will take time to materialise.

In all, China’s coal output and capacity will both keep growing during the 14th five-year plan period although we expect them to decline after 2025. More advanced mining technologies will support higher output, while the number of mines will be cut. The seasonal tightness and starker regional imbalance of coal supply will lead to greater exposure to market vulnerabilities. To mitigate the pressure, the industry will be at the hands of fewer prominent producers. Also, China is expanding its coal inventory capability to ease temporary shortages and price volatility.

Source: Wood Mackenzie